24 / 372

24 / 372

審計人員之產業專精與客戶租稅規避:中國實證研究

24

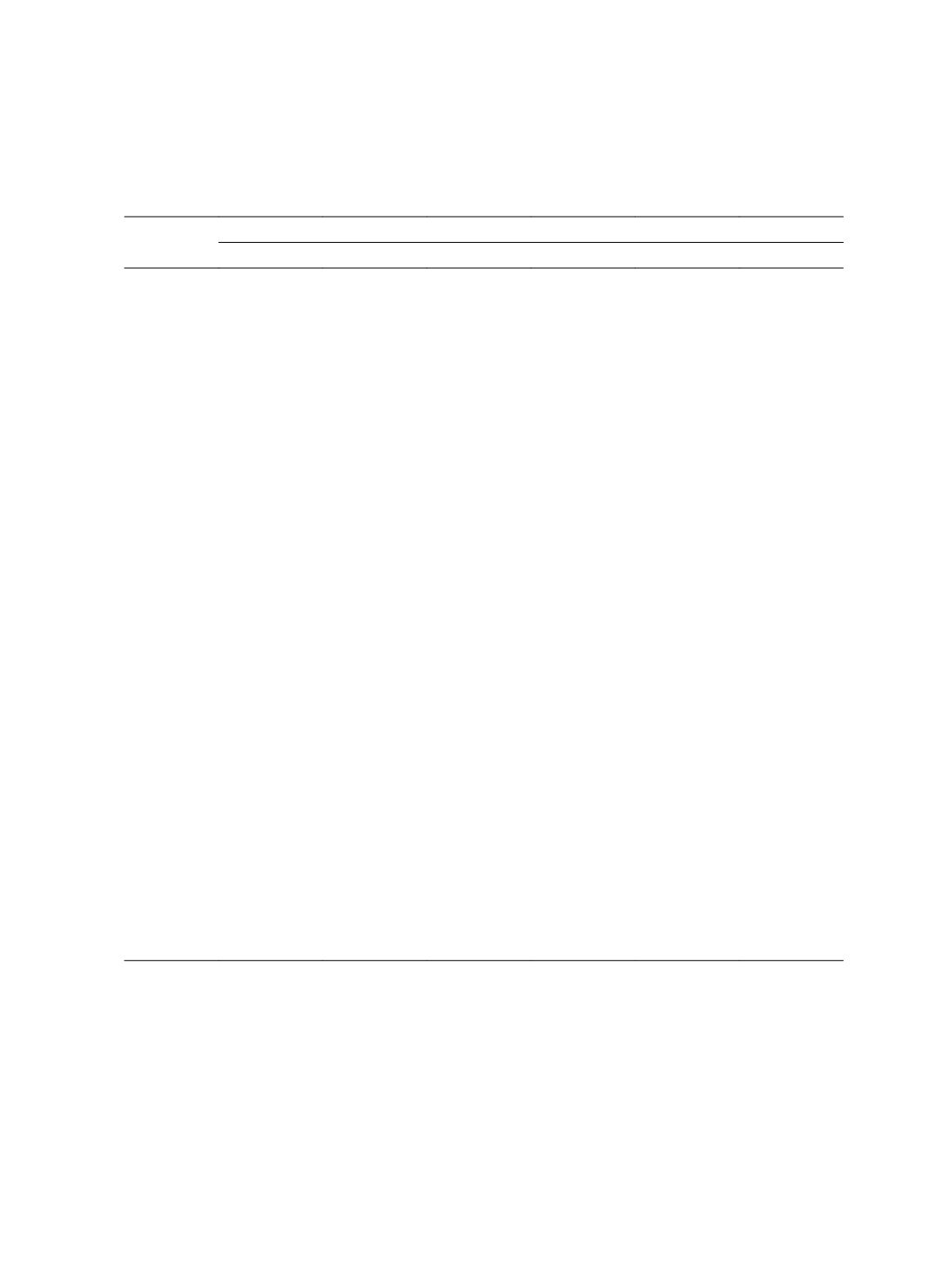

Table 9 Association between Auditor Industry Expertise and Tax Avoidance in Big 4

Sample

Variables

(1)

Tax-avoidance = BETR

(2)

Tax-avoidance = CETR

(3)

Tax-avoidance = BTD

Spec = IMS Spec = IPS Spec = IMS Spec = IPS Spec = IMS Spec = IPS

Constant

-0.1187*

-0.1309*

-0.1505

-0.1583

0.7748

0.8693

(-1.84)

(-1.88)

(-1.31)

(-1.37)

(0.46)

(0.51)

Spec

-0.0158*

-0.1105**

-0.0133

-0.0270

0.2399*

0.3715

(-1.76)

(-2.18)

(-0.91)

(-0.41)

(1.72)

(0.38)

Fee

-0.4487

-0.6660*

-0.9655*

-1.0307*

5.6625

5.2720

(-1.14)

(-1.66)

(-1.89)

(-1.96)

(0.75)

(0.68)

Tenure

-0.0073

-0.0015

0.0011

0.0007

0.0212

0.0080

(-0.84)

(-1.00)

(0.52)

(0.34)

(0.72)

(0.27)

Spec*Fee

-0.2608

-1.2158

-2.6945**

-2.9287**

5.6392

8.8386

(-0.26)

(-1.12)

(-2.09)

(-2.07)

(0.30)

(0.43)

Spec*Tenure

-0.0093

0.0081

-0.0074

-0.0024

0.1988*

0.0638

(-1.01)

(-1.02)

(-0.62)

(-0.23)

(1.71)

(0.42)

Soe

-0.0203**

-0.0187**

0.0046

0.0030

0.5521***

0.5241***

(-2.12)

(-1.97)

(0.37)

(0.24)

(3.01)

(2.89)

Size

0.0082**

0.0082**

0.0008

0.0010

0.7823***

0.7875***

(2.17)

(2.19)

(0.16)

(0.21)

(10.82)

(10.89)

Roa

0.0084

0.0118

0.3638***

0.3629***

5.8170***

5.8278***

(0.08)

(0.11)

(2.68)

(2.67)

(2.92)

(2.93)

Lev

-0.0213

-0.0288

0.0587

0.0629*

1.2368**

1.2501**

(-0.73)

(-0.99)

(1.55)

(1.68)

(2.23)

(2.24)

CFO

0.0086

0.0130

0.0413

0.0405

0.4436

0.4675

(0.15)

(0.24)

(0.55)

(0.53)

(0.40)

(0.42)

Year

Controlled

Controlled

Controlled

Controlled

Controlled

Controlled

Industry

Controlled Controlled Controlled Controlled Controlled Controlled

N

455

455

455

455

455

455

F Value

7.41

7.84

4.76

4.74

29.10

29.03

Adjusted R

2

0.2075

0.2128

0.1105

0.1091

0.5606

0.5596

Note: This table presents the OLS regression results in Big 4 sample. Since Big 4 are more likely to be

identified as experts based on dummy variables (

IMS_D

and

IPS_D

equal 1 in most of Big 4

sample observations), we only use continuous variables (

IMS

and

IPS

) to proxy industry

expertise. The sample includes 455 firm-year observations for the period 2008-2012. T-statistics

are in the parentheses. ***, **, * stand for a statistical significant level of 1%, 5%, and 10%

respectively.