324 / 414

324 / 414

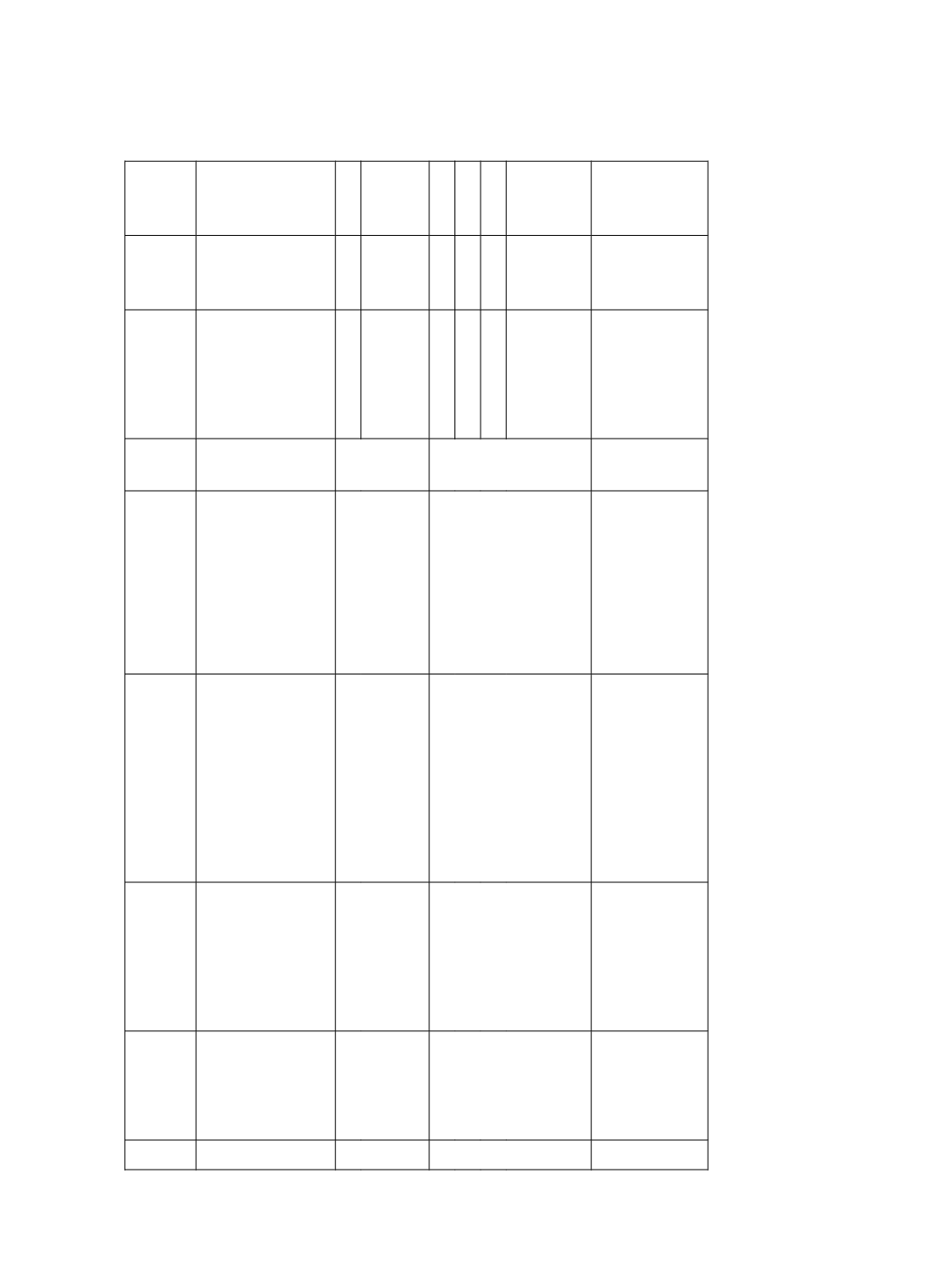

亞洲地區審計品質研究回顧

324

國

家

證券主管機關 審計主管機關 會計準則制訂機關 審計準則制訂機關

是否

加入

IFIAR

交易所

上市公司

家數

(12

/ 2014)

市值十億

美金

(12

/ 2014)

南

韓

Financial

Supervisory

Service

Financial

Supervisory

Service

(隸屬

Financial

Services

Commission

)

Korean Accounting Institute

(KAI)

(歸屬於獨立機構)

2011

年強制適用

IFRS

Korean Institute of

Certified Public

Accountants

(歸屬會計專業團體

)

是

南韓證券期貨交

易所

1,864 1,212.8

中

國

China

Securities

Regulatory

Commission

Ministry of Finance

(MOF)

Ministry of Finance

(歸屬於政府)

2007

年起會計準則與

IFRS

趨同

The Chinese Institute of

Certified Public

Accountant (CICAP)

(歸屬於會計專業團體)

否

上海證券交易所

995 3,932.5

深圳證券交易所

1,618 2,072.4

日

本

Financial

Services

Agency

Certified Public

Accountants &

Auditing Oversight

Board

(隸屬

Financial

Services Agency

)

Financial Accounting

Standards Foundation

(FASF)

(歸屬於獨立機構)

與

IFRSs

趨同,符合條件之

日本上市公司可自願性適用

IFRSs

Financial Services

Agency/ Japan Institute

of Certified Public

Accountant (JICPA)

(政府

/

會計專業團體

)

是

東京證券交易所

3,470 4,378.0

名古屋證券交易所

298 1,288.7

札幌證券取引所

56

440.6

福岡證券取引所

114*

536.1

以

色

列

Israel

Securities

Authority

(ISA)

Israel Securities

Authority (ISA)

Israel Accounting Standards

Board

(歸屬於獨立機構)

上市公司

2008

年後適用

IFRSs

Institute of Certified

Public Accountants in

Israel

(歸屬會計專業團體)

否

特拉維夫證券交

易所

473 200.5

註一:

IFIAR

全稱為

International Forum of Independent Audit Regulators (IFIAR)

。

註二:交易所資料取自

World Federation of Exchanges

。日本札幌證券取引所(亦即臺灣所稱之交易所)、福岡證券取引所與巴基斯坦三個交易

所之資料取自交易所網頁。

註三:國際會計準則採用狀況統計自

Deloitte

網頁

: http://www.iasplus.com/en/jurisdictions

。最後搜尋時間為:

2015

年

4

月

30

日。