311 / 414

311 / 414

臺大管理論叢

第

27

卷第

1

期

311

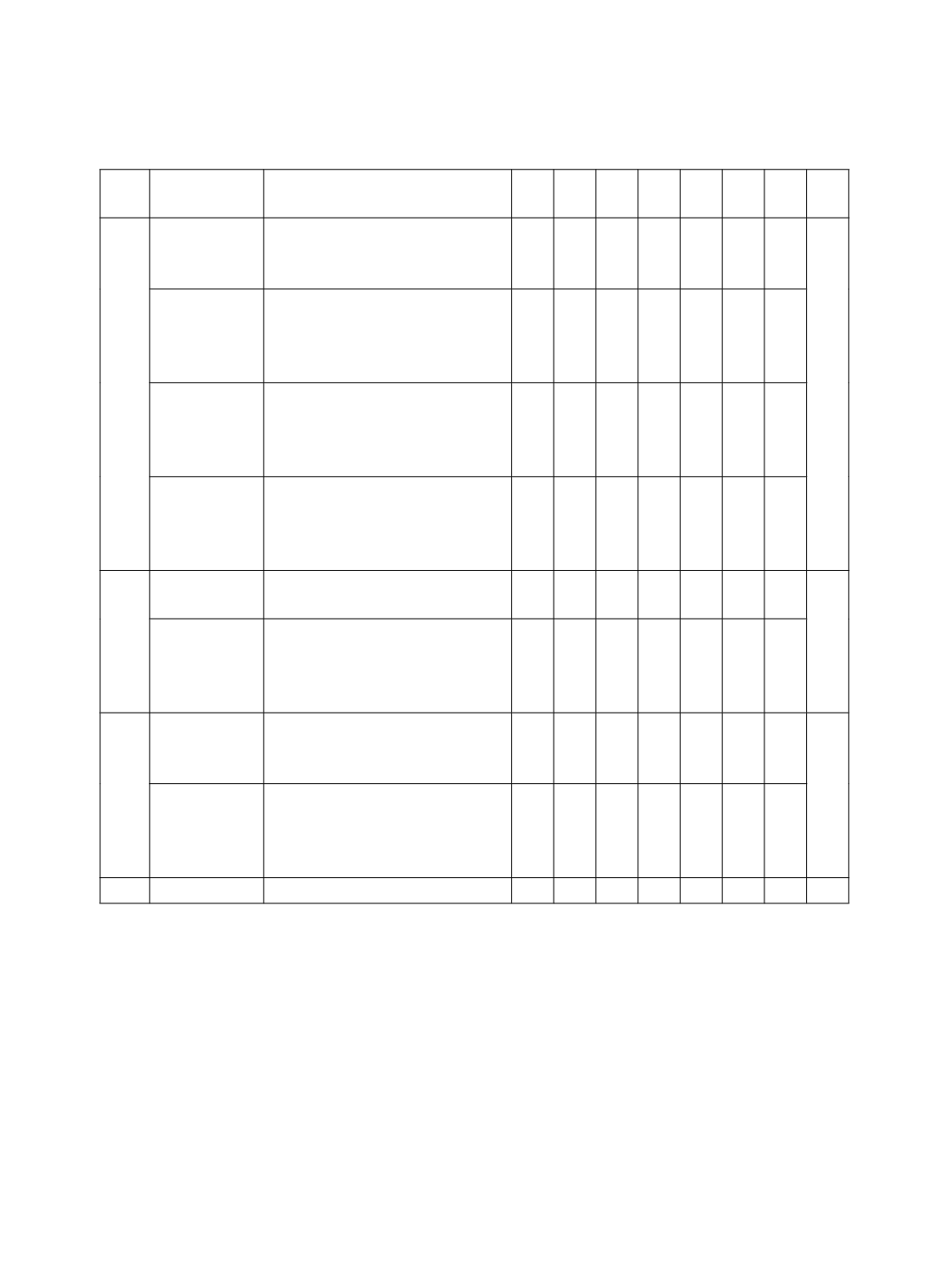

期刊 作者

標題

中國 臺灣 南韓 香港 日本 伊朗

馬來

西亞

合計

Chi and Chin

(2011)

Firm versus partner measures of

auditor industry expertise and

effects on auditor quality

1

Chan, Lin, and

Wang (2012)

Government ownership,

accounting-based regulations,

and the pursuit of favorable audit

opinions: Evidence from China.

1

Kwon, Lim,

and Simnett

(2014)

The effect of mandatory audit firm

rotation on audit quality and audit

fees: Empirical evidence from the

Korean audit market.

1

Wang, Yu, and

Zhao (2015)

The association between audit-

partner quality and engagement

quality: Evidence from financial

report misstatements.

1

AH

Xiao, Zhang,

and Xie (2000)

The making of independent

auditing standards in China

1

2

Chin, Yao, and

Liu (2014)

Industry audit experts and

ownership structure in the

syndicated loan market: At the

firm and partner Levels

1

EAR

Wang, Liu,

and Chang

(2011)

CPA-firm merger: An investigation

of audit quality.

1

2

He, Pan, and

Tian (2015)

Legal liability, government

intervention, and auditor behavior:

Evidence from structural reform of

audit firms in China

1

合計

28 8 3 2 2 1 1 45

*

本篇文章除正文

(Lam and Mensah, 2006a)

外,還有

LaSalle (2006)

之評論與

Lam and Mensah

(2006b)

評論意見回覆等共計

3

篇。