309 / 414

309 / 414

臺大管理論叢

第

27

卷第

1

期

309

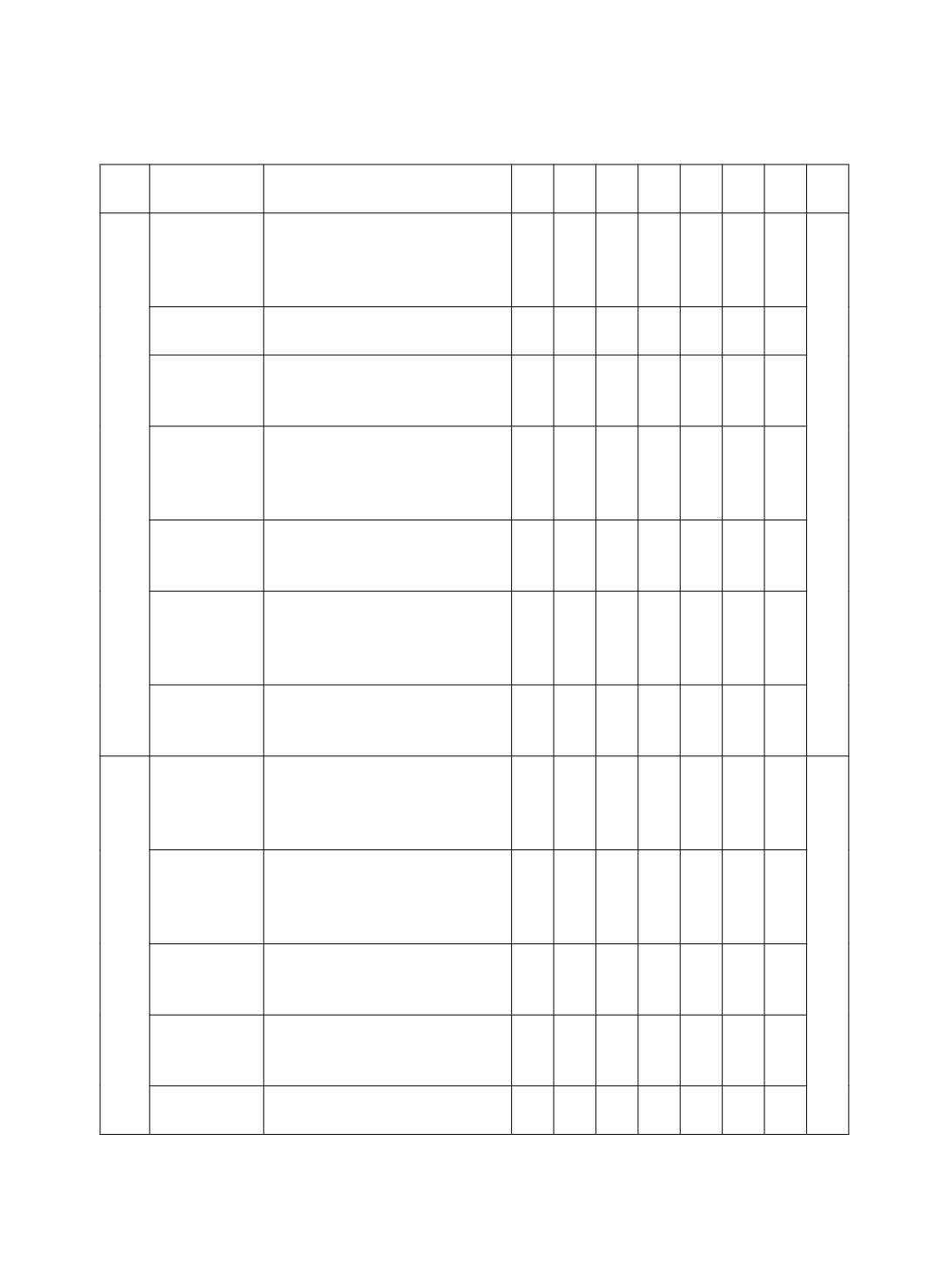

期刊 作者

標題

中國 臺灣 南韓 香港 日本 伊朗

馬來

西亞

合計

CAR

Chi, Huang,

Liao, and Xie

(2009)

Mandatory audit partner rotation,

audit quality, and market

perception: Evidence from

Taiwan.

1

Chin and Chi

(2009)

Reducing restatements with

increased industry expertise.

1

Kim, Simunic,

Stein, and Yi

(2011)

Voluntary audits and the cost of

debt capital for privately held

firms: Korean evidence.

1

Chen, Chen,

Lobo, and

Wang (2011)

Effects of audit quality on

earnings management and cost of

equity capital: Evidence from

China.

1

Chan and Wu

(2011)

Aggregate quasi rents and auditor

independence: Evidence from

audit firm mergers in China.

1

Firth, Mo, and

Wong (2012)

Auditors’ organizational form,

legal liability, and reporting

conservatism: Evidence from

China.

1

Yang (2013)

Do political connections add value

to audit firms? Evidence from IPO

audits in China.

1

JAPP

Lam and

Mensah

(2006a)

Auditors’ decision-making under

going-concern uncertainties in low

litigation-risk environments:

Evidence from Hong Kong.

1*

9

Zhou (2007)

Auditing standards, increased

accounting disclosure, and

information asymmetry: Evidence

from an emerging market.

1

Kim and

Cheong

(2009)

Does auditor designation by the

regulatory authority improve audit

quality? Evidence from Korea.

1

Chi, Douthett,

and Lisic

(2012)

Client importance and audit

partner independence.

1

Firth, Rui, and

Wu (2012)

Rotate back or not after

mandatory audit partner rotation?

1