310 / 414

310 / 414

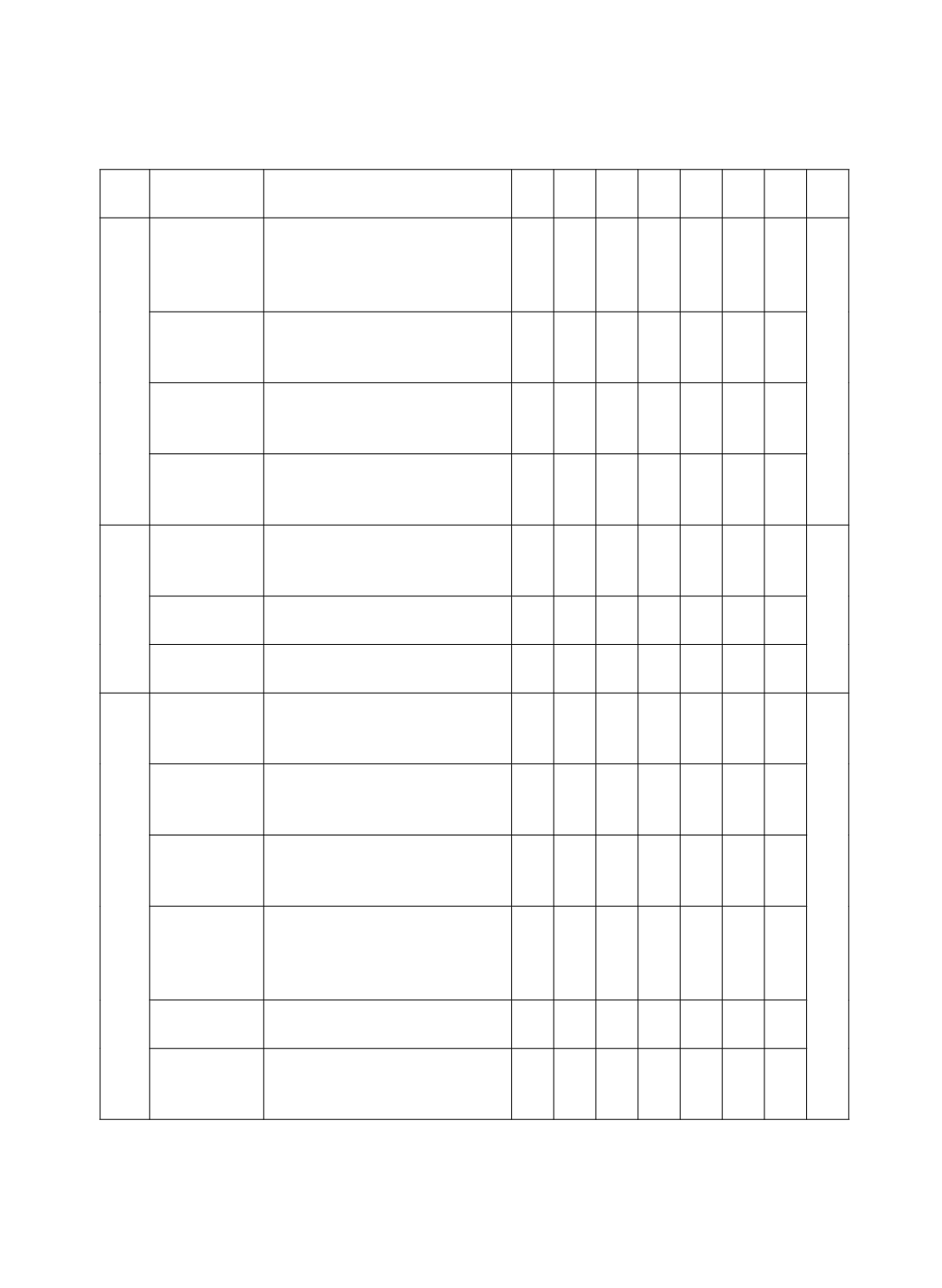

亞洲地區審計品質研究回顧

310

期刊 作者

標題

中國 臺灣 南韓 香港 日本 伊朗

馬來

西亞

合計

JAPP

Chi, Lisic,

Long, and

Wang (2013)

Do regulations limiting

management influence over

auditors improve audit quality?

Evidence from China.

1

Liu and

Subramaniam

(2013)

Government ownership, audit firm

size and audit pricing: Evidence

from China.

1

He, Rui,

Zheng, and

Zhu (2014)

Foreign ownership and auditor

choice.

1

Bagherpour,

Monroe, and

Shailer (2014)

Government and managerial

influence on auditor switching

under partial privatization.

1

JAAF

Gul, Sun, and

Tsui (2003)

Tracks: Audit quality, earnings,

and the Shanghai stock market

reaction.

1

3

Haw, Qi, and

Wu (2008)

The economic consequence of

voluntary auditing.

1

Saito and

Takeda (2014)

Global audit firm networks and

their reputation risk.

1

AJPT

DeFond,

Francis, and

Wong (2000)

Auditor industry specialization

and market segmentation:

Evidence from Hong Kong.

1

10

Chen, Chen,

and Su (2001)

Profitability regulation, earnings

management, and modified audit

opinions: Evidence from China.

1

Haw, Park, Qi,

and Wu (2003)

Audit qualification and timing of

earnings announcements:

Evidence from China.

1

Chen, Su, and

Wu (2009)

Forced audit firm change,

continued partner-client

relationship, and financial

reporting quality.

1

Gul, Sami, and

Zhou (2009)

Auditor disaffiliation program in

China and auditor independence.

1

Chen, Su, and

Wu (2010)

Auditor changes following a Big 4

merger with a local Chinese firm:

A case study.

1