Page 218 - 32.3

P. 218

Earnings Management Behavior under the Global Budget Payment and Reduction of Medical Expenses

System: The Effects of Different Types of Hospitals

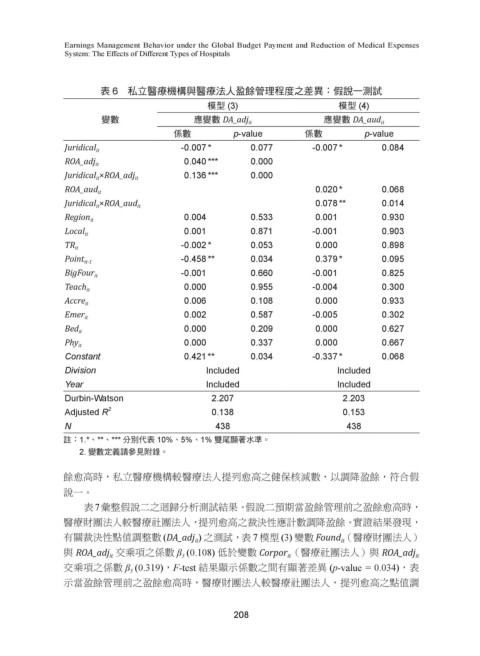

表 6 私立醫療機構與醫療法人盈餘管理程度之差異:假說一測試

模型 (3) 模型 (4)

變數 應變數 DA_adj it 應變數 DA_aud it

係數 p-value 係數 p-value

Juridical it -0.007 * 0.077 -0.007* 0.084

0.040 *** 0.000

ROA_adj it

0.136 *** 0.000

Juridical it ×ROA_adj it

ROA_aud it 0.020 * 0.068

0.078 ** 0.014

Juridical it ×ROA_aud it

0.004 0.533 0.001 0.930

Region it

Local it 0.001 0.871 -0.001 0.903

-0.002 * 0.053 0.000 0.898

TR it

-0.458 ** 0.034 0.379 * 0.095

Point it-1

BigFour it -0.001 0.660 -0.001 0.825

0.000 0.955 -0.004 0.300

Teach it

0.006 0.108 0.000 0.933

Accre it

0.002 0.587 -0.005 0.302

Emer it

0.000 0.209 0.000 0.627

Bed it

0.000 0.337 0.000 0.667

Phy it

Constant 0.421** 0.034 -0.337* 0.068

Division Included Included

Year Included Included

Durbin-Watson 2.207 2.203

Adjusted R 2 0.138 0.153

N 438 438

註:1.*、**、*** 分別代表 10%、5%、1% 雙尾顯著水準。

2. 變數定義請參見附錄。

餘愈高時,私立醫療機構較醫療法人提列愈高之健保核減數,以調降盈餘,符合假

說一。

表7彙整假說二之迴歸分析測試結果。假說二預期當盈餘管理前之盈餘愈高時,

醫療財團法人較醫療社團法人,提列愈高之裁決性應計數調降盈餘。實證結果發現,

有關裁決性點值調整數 (DA_adj ) 之測試,表 7 模型 (3) 變數 Found (醫療財團法人)

it

it

與 ROA_adj 交乘項之係數 β (0.108) 低於變數 Corpor (醫療社團法人)與 ROA_adj it

it

it

3

交乘項之係數 β (0.319),F-test 結果顯示係數之間有顯著差異 (p-value = 0.034),表

5

示當盈餘管理前之盈餘愈高時,醫療財團法人較醫療社團法人,提列愈高之點值調

208