182 / 322

182 / 322

期貨未平倉量的資訊內涵及其交易活動之研究

182

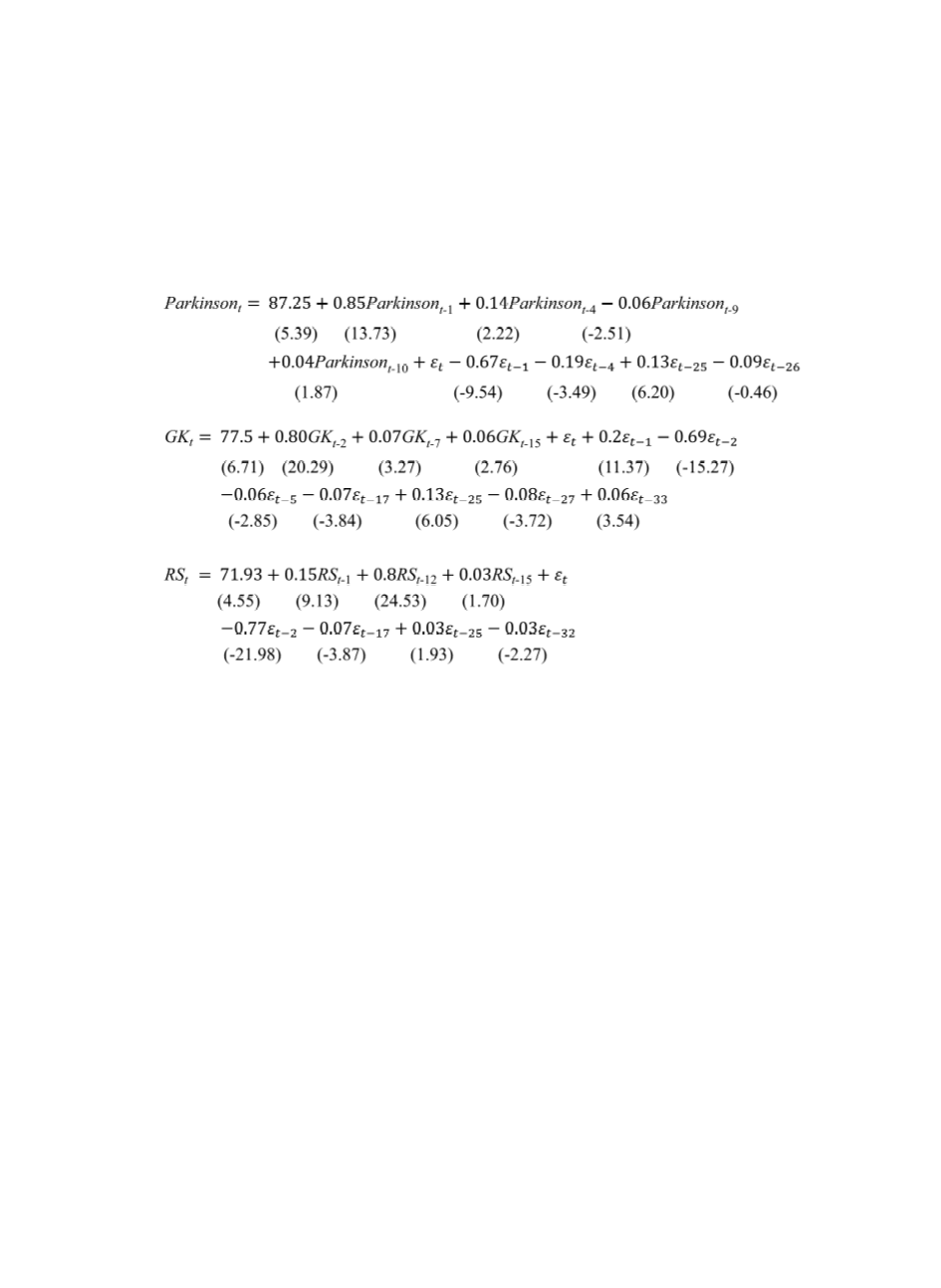

Appendix B

The three volatility proxies are identified by ARIMA models with the following

parameter estimates:

Numbers in parentheses are t-statistics. All coefficients are significant at the 5% level.

None of the Ljung-Box Q-statistics for lag lengths 1-60 are significant at the 5% level.