276 /304

276 /304

沙賓法

404

條及審計準則第

5

號是否會減少內部控制揭露錯誤?

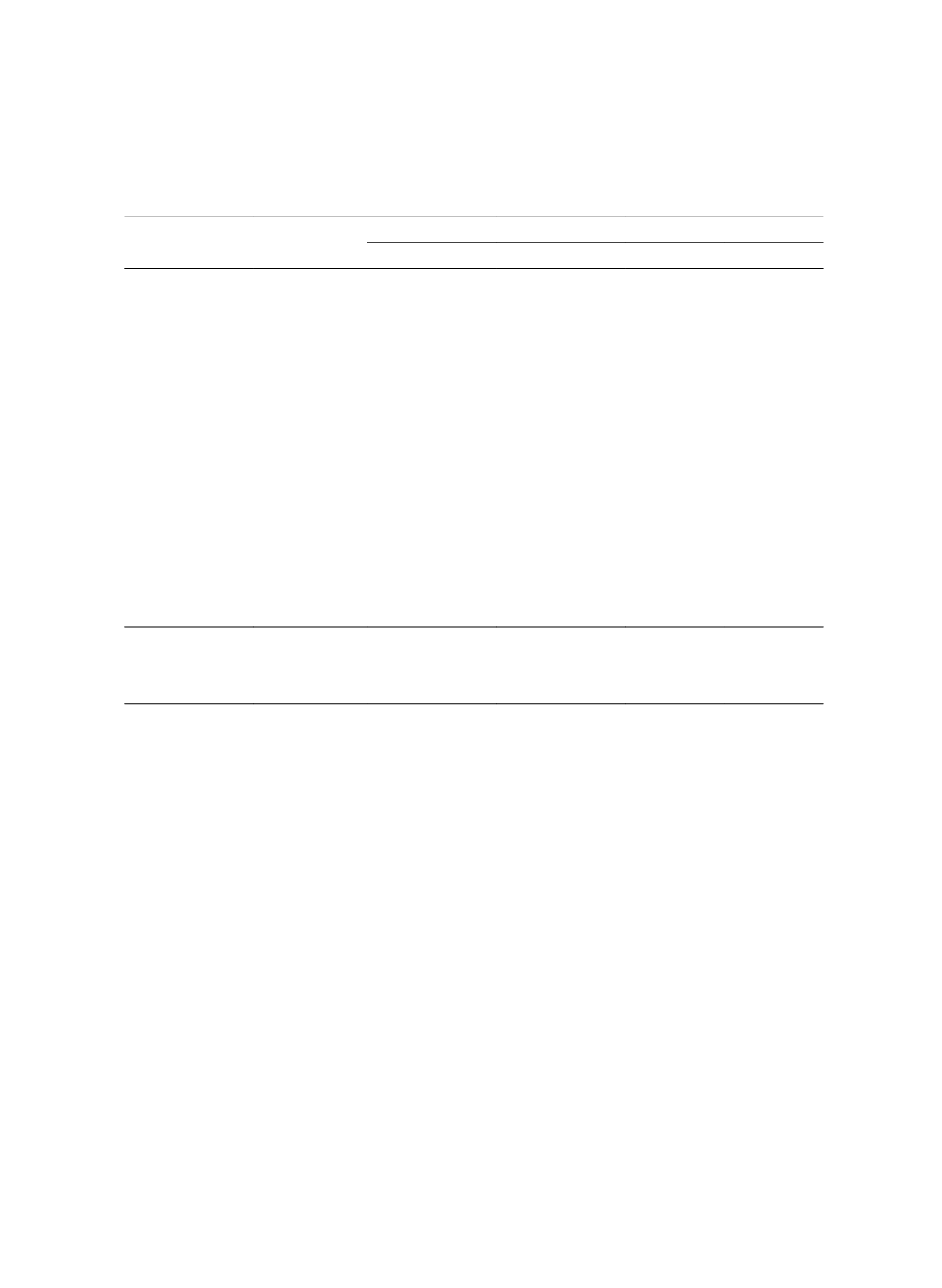

276

Table 7 Logistic Regression for Restatement and Non-restatement Samples

(Dependent Variable =

EFFECTIVE

)

Predicted Sign

Restatement Sample

Non-restatement Sample

Coefficient

p-value

Coefficient

p-value

SOX404

?

-0.932

0.046

-0.682

0.204

SIZE

+

0.075

0.306

0.008

0.918

ROA

+

0.224

0.697

-0.466

0.351

LEV

-

-0.225

0.395

-0.146

0.579

PE

-

0.000

0.914

-0.003

0.077

MB

-

0.010

0.565

0.046

0.013

BIGN

?

0.283

0.259

0.592

0.003

RCP

-

-0.006

0.062

-0.007

0.023

FT

-

-0.356

0.051

-0.285

0.096

AGLOSS

-

-0.503

0.010

-0.715

<0.001

MARKETCAP

+

0.000

0.246

0.000

<0.001

CONSTANT

2.689

0.034

18.164

0.982

YEAR

(include)

(include)

INDUSTRY

(include)

(include)

LR chi squared

271.78

<0.001

272.12

<0.001

Pseudo R

2

0.172

0.132

Sample size

1853

10774

Note: Variables are defined in Table 2. P-values are based on two-tailed tests.

Table 8 presents the results of applying Model 2 to the subsample of the SOX 404

era. For the restatement sample, the coefficient on

AS5

is 1.413, with a p-value < 0.001,

indicating that the odds of concluding that internal controls are effective for restatement

companies adopting AS5 increases by 411.16%, compared with their restatement

counterparts adopting AS2. This result suggests that the implementation of AS5 has

resulted in a higher Type II error rate. For the non-restatement sample, the coefficient on

AS5

is 1.418, with a p-value < 0.001, indicating that the odds of concluding that internal

controls are effective for non-restatement companies adopting AS5 increased by 412.79%,

compared with the odds of their non-restatement counterparts concluding the same while

adopting AS2. This finding is consistent with our H2b, and it suggests that implementation

of AS5 could improve ICFR-audit efficiency by reducing Type I errors. To sum up, our

evidence shows that even though the more flexible and less prescriptive AS5 can enhance

the efficiency of ICFR audits, it inadvertently lowers public ICFR-disclosure quality,

measured as Type II errors.