42 / 414

42 / 414

服務主導邏輯之共同生產:前置因素與結果因素

42

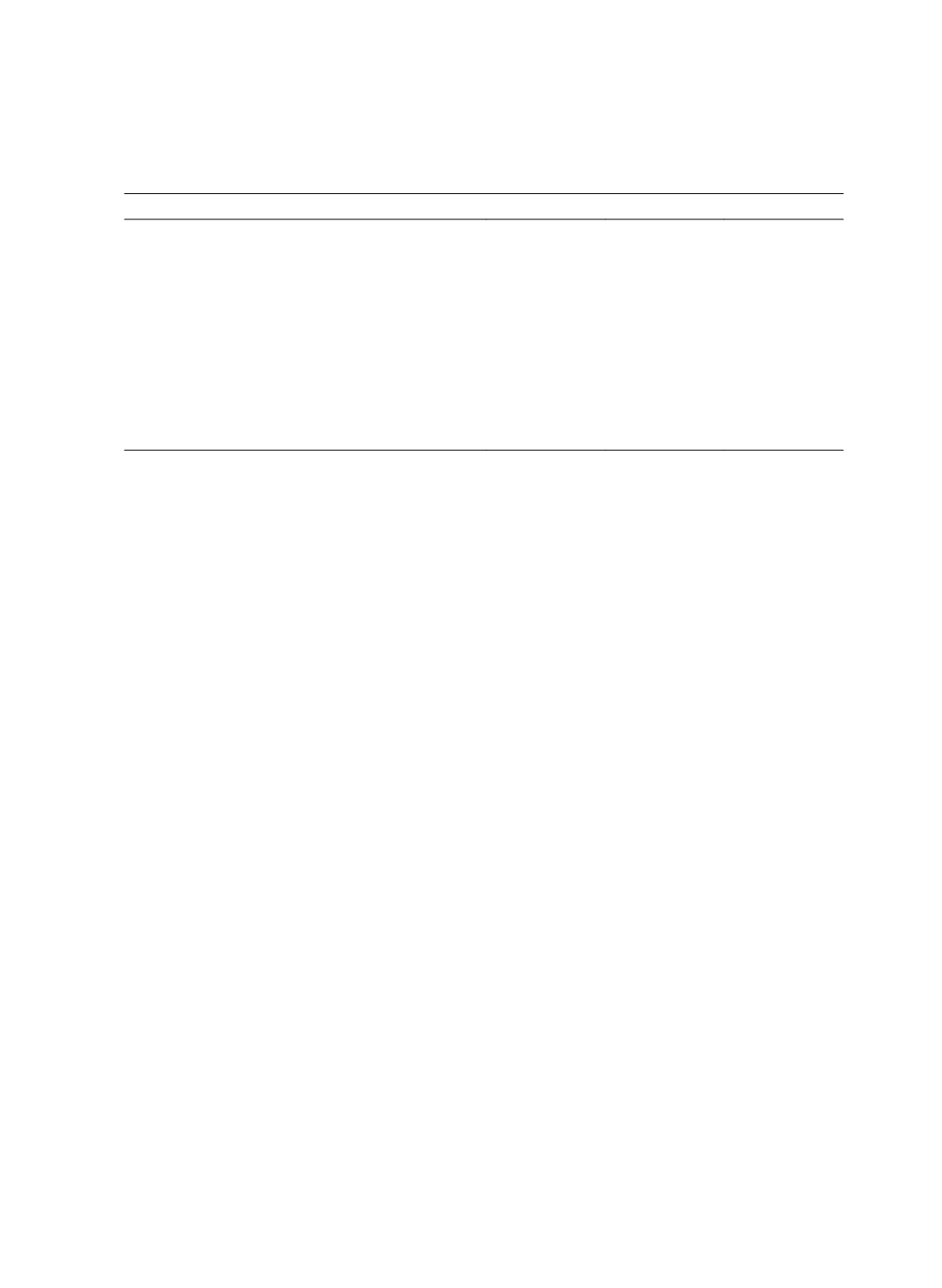

Table 2 LISREL Results

Proposed path

H

Coefficient

t

Asset Specificity

→

Co-production

H1

0.279*

4.587

Quality of Customer Interaction

→

Co-production

H2

0.172*

2.645

Decision-making Uncertainty

→

Co-production

H3

0.231*

4.171

Co-production

→

Special Treatment Benefits

H4

0.181*

2.709

Co-production

→

Social Benefits

H5

0.353*

6.229

Co-production

→

Confidence Benefits

H6

0.229*

4.378

Special Treatment Benefits

→

Share of Wallet

H7

0.068*

8.057

Social Benefits

→

Share of Wallet

H8

0.030*

3.194

Confidence Benefits

→

Share of Wallet

H9

0.055*

5.282

Note: *

p

< 0.05.

4.3 Additional Analyses

Firm size may be a potential moderator. In general, larger firms have an advantage over

smaller firms as the former provides one-stop shopping, which reduces the search cost for

customers and takes advantage of share of wallet from existing customers. In this study, the

total sample was divided into two groups according to whether the bank is based on a

financial holding company (large firm size) or not (small firm size). Finally, the sample size

was n = 271 for financial holding company-based banks, and n = 135 for non-financial

holding company-based banks. Then, the different effects of relational benefits on share of

wallet were investigated. Results showed that the effect of special treatment benefits on share

of wallet was stronger under financial holding company-based banks (

β

= 0.079,

p

< 0.05)

than under non-financial holding company-based banks (

β

= 0.042,

p

< 0.05). Such a result

can be attributed to the fact that the former can fully capitalize on cross-selling various

product categories, and thus easily tailor the products to the specific needs of each customer.

In addition, the effect of confidence benefits on share of wallet was stronger under financial

holding company-based banks (

β

= 0.072,

p

< 0.05) than under non-financial holding

company-based banks (

β

= 0.024,

p

< 0.05). The size of the firm provides important

information to customers that firms can be trusted because large firms are perceived as more

confident, reliable, and trustworthy than small ones. Instead, the effect of social benefits on

share of wallet was stronger under non-financial holding company-based banks (

β

= 0.057,

p

< 0.05) than under financial holding company-based bank (

β

= 0.016,

p

> 0.05). Given that

the former are mostly found in less strong financial and power positions than the latter, and

thus non-financial holding company-based banks must develop commercial friendships with